Expert Insights from: Ozkan Okumus, Former COO of Allianz, 20+ years in the insurance industry.

This article is part of Infoquest’s Expert Voices series, featuring editorial insights drawn from in-depth conversations with sector professionals across the globe. Infoquest connects organizations with the specialized expertise they need to make better decisions, faster.

For decades, insurance operated on a simple premise: something goes wrong, you file a claim, the company pays. It was a system built entirely around loss. But that model is changing at a pace the industry has never seen before, according to Ozkan Okumus, a leadership and transformation consultant with senior roles across Allianz, Zurich, Generali, and BBVA Insurance spanning the Middle East, Russia, Australia, and Turkey.

“We are not just underwriting risk anymore. We are managing relationships, experiences, and trust.”

Insurance has shifted from a reactive posture to a proactive one. Customers no longer accept slow claims processes, opaque policy terms, or products that feel generic. Insurers are responding with technology, behavioral data, and a fundamentally different relationship with risk.

The Personalization Shift

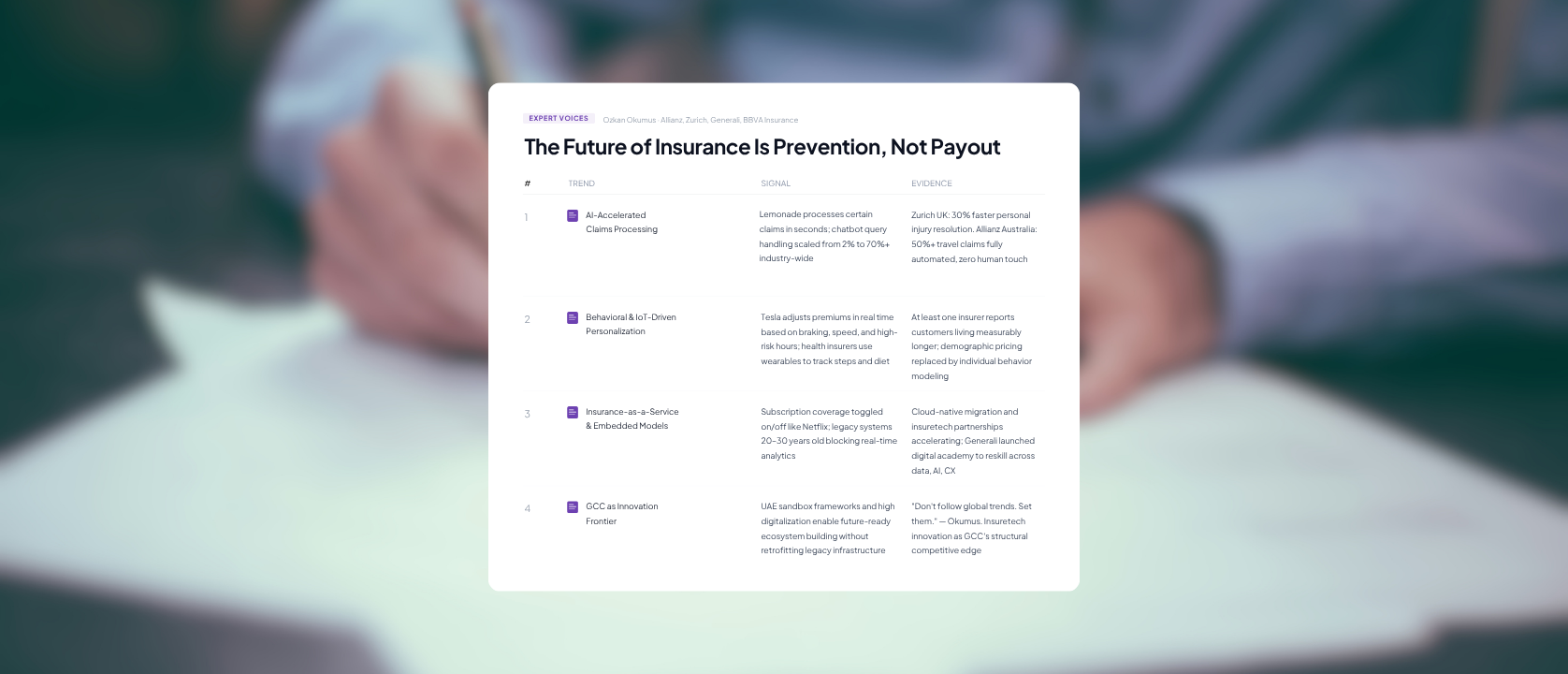

One of the clearest signals of this transformation is how products are being tailored to individual behavior rather than demographic categories. Tesla is a prominent example. The automaker now offers real-time rate adjustments based on how safely customers actually drive. Smooth braking, steady speeds, and avoiding high-risk hours all factor into the premium. If driving behavior deteriorates, the rate reflects that too.

The same logic is emerging in health and lifestyle coverage. Insurance companies are building products that track steps, diet, and daily habits through wearables, then adjusting premiums accordingly. Okumus notes that at least one of these companies claims its customers are living longer as a result, suggesting the model may be shifting outcomes, not just pricing.

“Personalization is no longer optional. It is expected. Today’s customers want products that reflect their lives, not just their demographic data.”

The engine behind this is data analytics combined with IoT. Insurers can now segment customers by behavior, risk tolerance, and engagement style, collecting real-time data through embedded devices and using it to dynamically price risk. Predictive analytics and gamification are helping insurers shift from selling policies to actively shaping healthier habits.

From Payers to Preventers

The most significant conceptual shift Okumus describes is the move from responding to losses to preventing them. Where insurers were once primarily payers, stepping in after something went wrong, they are now positioned to intervene before damage occurs.

AI is central to that shift. Across underwriting, claims, and customer service, artificial intelligence is compressing timelines and improving accuracy in ways that were unimaginable a decade ago. Lemonade, the AI-powered insuretech company, now processes certain claims in seconds. Zurich UK resolves personal injury claims 30% faster than traditional methods. At Allianz Australia, automated travel claims processing exceeded 50% without any human touch.

Customer-facing AI has followed a similar trajectory. Chatbots that handled roughly 2% of queries when first introduced in insurance now manage upwards of 70%, with services expanded to cover real-time claim filing, status tracking, and live agent escalation.

The challenges in getting there are real. Legacy systems, some 20 to 30 years old, were not designed for real-time analytics. Cultural inertia within large organizations slows adoption. And the competition for digital talent is intense. Insurers are responding by migrating to cloud-native platforms, partnering with insuretech firms, and reskilling workforces. Generali, for example, launched a digital academy to upskill employees across all functions in data, AI, and customer experience.

What the Next Decade Looks Like

Looking ahead, Okumus identifies three trends that will fundamentally reshape the industry. The first is real-time adaptive insurance, premiums that shift daily based on behavior, tied directly to IoT data from vehicles, wearables, and connected devices. The pricing model is no longer static. It responds.

The second is insurance-as-a-service: fully embedded, subscription-based models where coverage can be toggled on or off as needed. The flexibility consumers already expect from platforms like Netflix or Amazon is coming to insurance. When you need it, you turn it on. When you don’t, you turn it off.

The third, and perhaps most consequential, is AI-led risk prevention. The distinction matters. Previous models paid out when something bad happened. The new model works to stop the bad thing from happening at all.

“Insurers are becoming guardians of well-being, not just responders to losses. The shift is from protecting against the past to preventing future losses entirely.”

The GCC Opportunity

For organizations in the GCC specifically, Okumus sees a genuine competitive edge. The region’s high digitalization, government support for insuretech and fintech innovation, and sandbox frameworks such as those offered in the UAE create conditions where companies can build future-ready ecosystems quickly, rather than retrofitting legacy infrastructure that has held back incumbents in more mature markets.

His advice to the region runs in three directions: use regulation as a platform for innovation rather than a constraint; invest in digital-native talent, particularly younger professionals who are tech-savvy and motivated; and build ecosystems that connect government, insurers, startups, and universities.

“Don’t follow global trends. Set them.”

The industry is moving in one direction: toward personalization, prevention, and real-time responsiveness. The companies that will lead it are not those that manage claims most efficiently after the fact, but those that help customers avoid making claims in the first place.