Based on an Infoquest Expert Voices interview with a Senior Compliance Specialist, Saudi Banking Sector

Saudi banking compliance has never been more demanding. Regulatory expectations are shifting faster than most institutions anticipated, and the stakes for getting it wrong have grown considerably. A senior compliance specialist with deep experience across banking supervision and AML in the Kingdom shared a frank assessment of where Saudi banks are succeeding, where they are struggling, and what it takes to operate responsibly in today’s environment.

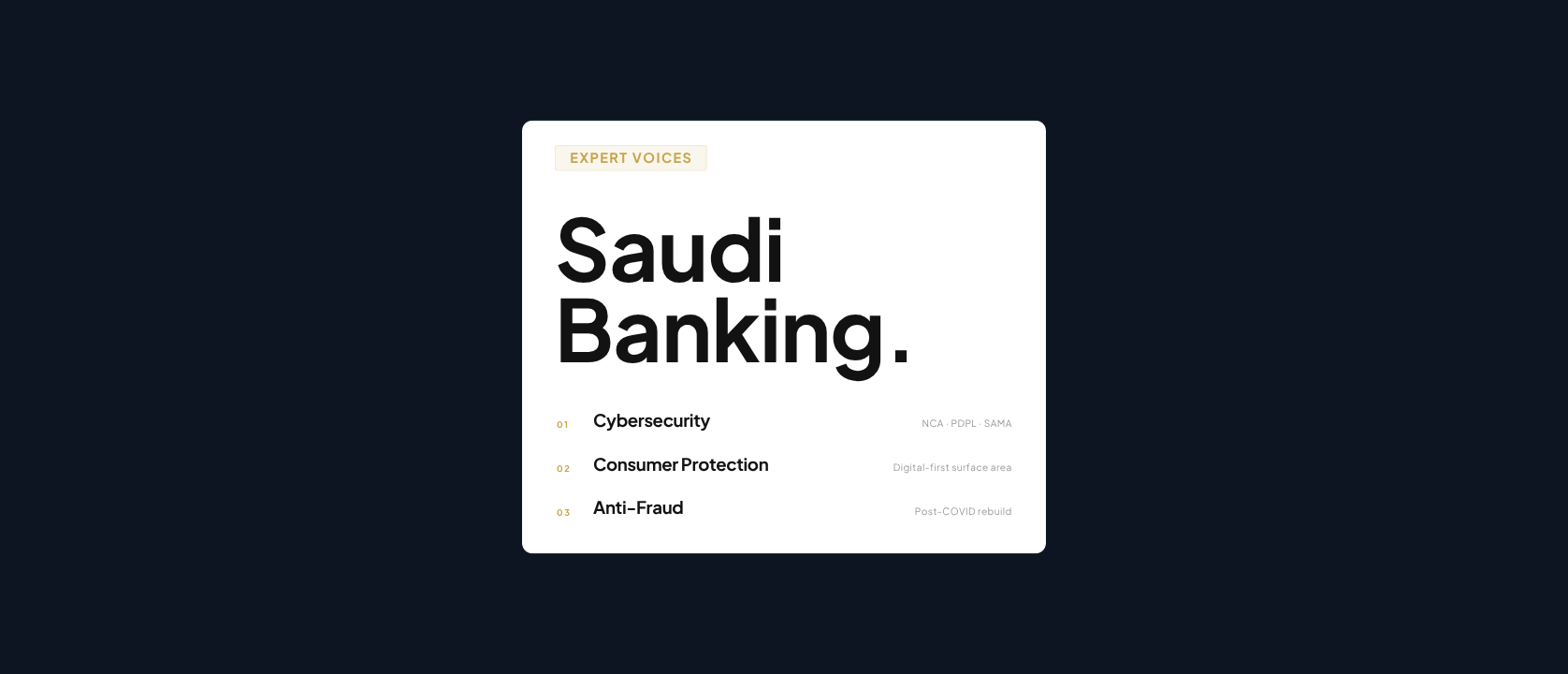

The Three Pillars of Saudi Banking Compliance

Ask any experienced compliance professional to name the most critical regulatory areas for Saudi banks, and three themes come up immediately: cybersecurity, consumer protection, and personal data protection. These are not abstract priorities. They reflect real, recent actions by SAMA and other Saudi regulatory bodies, and they are shaping how banks allocate resources, train staff, and design systems.

Cybersecurity has become a sharper regulatory focus as the National Cybersecurity Authority has issued its frameworks in recent years. Personal data protection followed with the introduction of Saudi Arabia’s Personal Data Protection Law, aligning the Kingdom broadly with international standards like the GDPR. Consumer protection has been a SAMA priority for longer, but it has intensified as digital banking expands the surface area of customer interactions.

Anti-Fraud Regulations Rebuilt After COVID-19

The anti-fraud landscape in Saudi Arabia has changed significantly since the pandemic. COVID-19 accelerated financial crime globally, and Saudi Arabia was not spared. A surge in social engineering attacks prompted SAMA to substantially update its anti-fraud framework, and banks have had to adapt quickly. The new regulations are detailed, and keeping pace with them requires both the right systems and the right people.

One element of anti-fraud compliance specific to Saudi Arabia is commercial concealment, the practice of conducting commercial activity under another party’s name or license. It is recognized as a distinct crime under Saudi law and sits within the compliance remit of banks operating in the Kingdom. It is the kind of nuanced, local regulatory context that compliance teams cannot afford to overlook.

Skilled Resources and Monitoring Systems Are the Core Gap

Understanding the regulatory framework is one challenge. Meeting it consistently is another. The most significant barrier to effective compliance is not awareness of regulations, but access to skilled human resources and capable monitoring systems.

Saudi banking compliance requires people who understand the specifics of SAMA’s expectations, can interpret new guidance quickly, and can design internal controls that hold up to inspection. Banks that have invested in this capacity, through experienced staff and transaction monitoring technology alike, are better positioned to handle regulatory change without disruption. Those who have not are exposed.

SAMA’s Sandbox Program: Structured Space for Innovation

SAMA is consistently described by practitioners as one of the stronger central banks in the GCC, and its approach to innovation reflects that. Rather than positioning regulation as a barrier to new products, SAMA has built a structured environment for testing them. The sandbox program allows banks and non-banks alike to develop and test new products under controlled conditions before bringing them to market.

The process is documented, with clear criteria, timelines, and communication protocols. Products that pass testing can proceed to launch. Those that do not are stopped before they reach customers. This framework has supported the licensing of digital banks in the Kingdom so far: STC Bank and Saudi Digital Bank. It is a model that protects consumers while giving institutions the space to compete.

Operating Across Saudi Arabia’s Multi-Regulator Landscape

SAMA is the primary regulator for Saudi banks, but it operates within a broader regulatory ecosystem. Banks in the Kingdom are accountable to multiple authorities depending on the nature of their activities. The Capital Market Authority governs listed entities. The Ministry of Commerce oversees commercial registration. The Ministry of Investment is relevant for foreign branches. Personal data falls under the Saudi Data and Artificial Intelligence Authority. AML and counter-terrorist financing compliance intersect with national security bodies.

For banks and fintechs building solutions for the Saudi market, this multi-regulator landscape is not optional knowledge. Understanding which authority applies to which activity, and maintaining appropriate relationships with each, is part of what effective compliance looks like in practice.

Three Rules for Getting Saudi Banking Compliance Right

The expert offers direct advice for anyone building solutions in the Saudi banking market. First, know your organization and define clear goals before approaching any regulatory framework. Second, comply not just with SAMA but with all relevant authorities in the Kingdom. Third, embed consumer protection and transparency into product design from the start, not as an afterthought.

Saudi banking compliance is demanding by design. SAMA wants a financial sector that is resilient, innovative, and trustworthy. The banks and fintechs building toward all three are the ones best placed to grow in one of the region’s most dynamic markets.