Based on an Infoquest Expert Voices interview with Ozkan Okumus, Insurance Transformation Leader

The insurance industry has long been synonymous with paperwork, waiting, and fine print. But AI in the insurance industry is rewriting that script, turning a sector built on historical data and reactive payouts into one that anticipates risk, personalizes coverage, and resolves claims in seconds. Ozkan Okumus, an insurance transformation leader who has worked across Allianz, Zurich, BBVA Insurance, and Sigma in markets spanning the Middle East, Europe, Russia, and Australia, has watched this shift unfold from inside some of the world’s largest insurers.

From Risk Underwriting to Relationship Management

The transformation, Okumus explains, runs deeper than technology upgrades. Over the past decade, insurance has moved from being purely reactive, stepping in only when something goes wrong, to becoming genuinely proactive and customer-centric. The industry’s mandate has expanded beyond underwriting risk. Insurers now see themselves as managers of relationships, experiences, and trust.

The inflection point came with the rise of insuretech. Lemonade, an AI-powered insurance company, now processes claims in seconds, something that would have seemed unimaginable a decade ago. That speed signals a broader structural shift: the expectation that everything in insurance should be real-time, online, and instant.

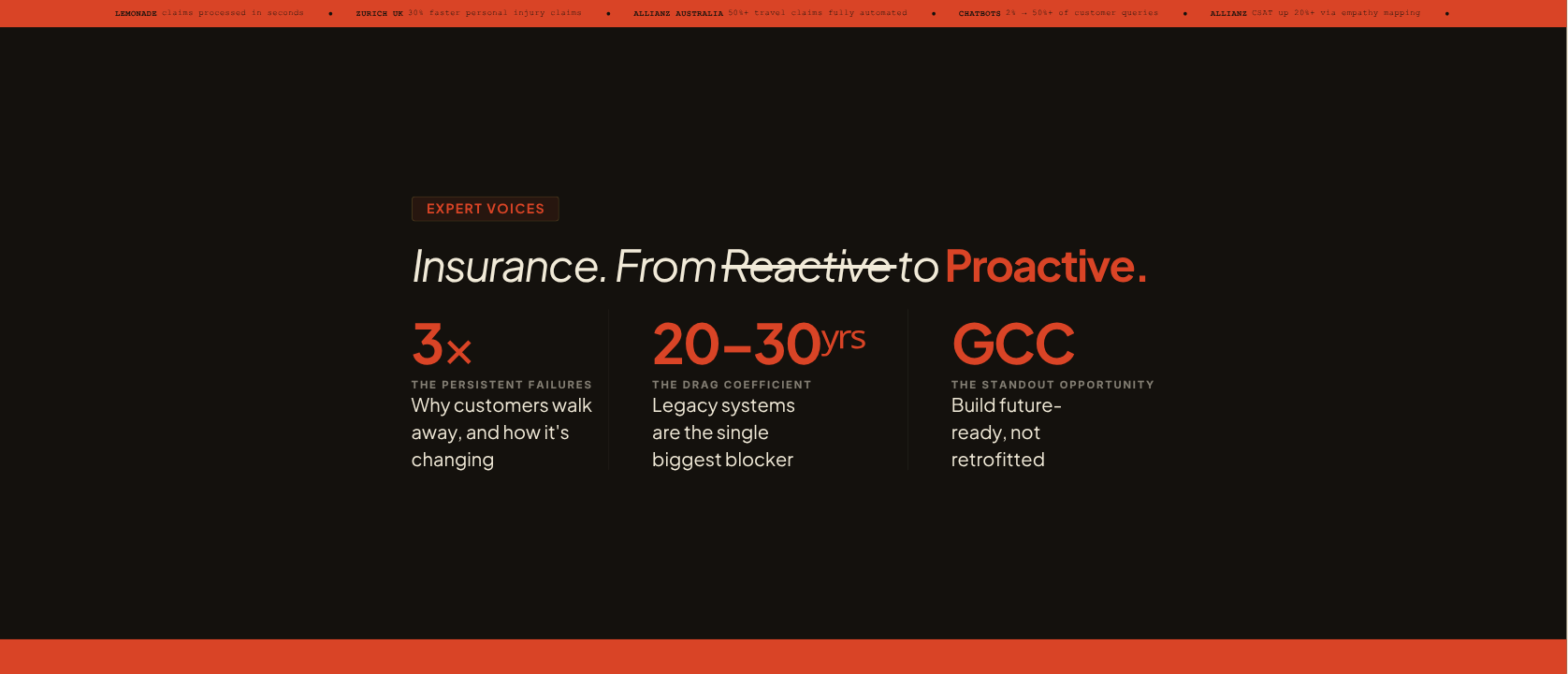

Three Reasons Customers Walk Away, and How That Is Changing

Customer dissatisfaction in insurance tends to cluster around three persistent failures. First, lack of transparency: many policyholders don’t understand what they’re covered for until it’s too late. Second, slow claims settlement: when people are most vulnerable, they run into bureaucracy. Third, impersonal service: insurance can feel transactional and cold, with little sense that the insurer knows or cares about the individual.

Insurers are tackling these failures with human-centric design. Allianz redesigned its claims process using empathy mapping, which pushed customer satisfaction scores up by more than 20%. The AXA app and Allianz’s mobile platform now let customers file claims, check status in real time, and chat with agents directly, cutting friction at the moments that matter most.

How AI in the Insurance Industry Is Changing Claims Forever

Artificial intelligence is reshaping three core functions: underwriting, claims processing, and customer service. AI models can assess risk profiles in seconds using live data. Computer vision analyzes vehicle damage while natural language processing scans hospital bills and supporting documents, all without human intervention.

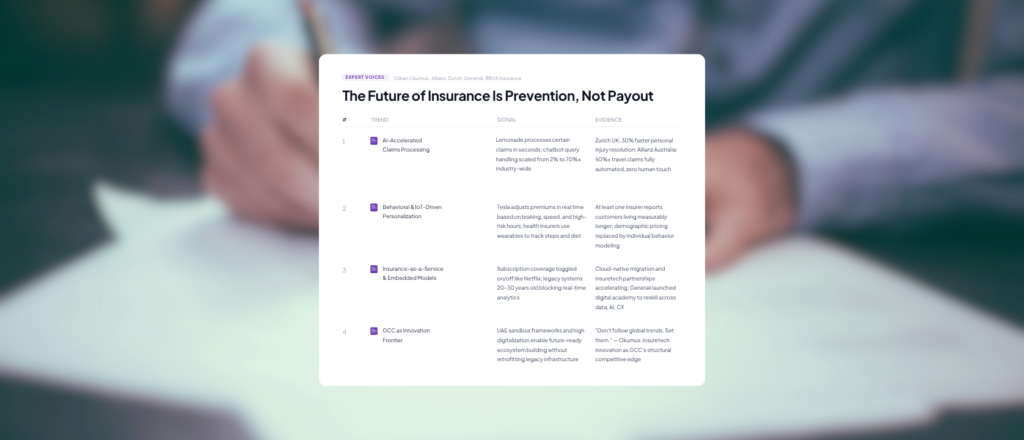

The numbers are striking. Chatbots now handle more than half of customer queries, up from roughly 2% when Okumus helped deploy early chatbot systems in the life insurance sector. Zurich UK processes personal injury claims 30% faster using AI. Allianz in Australia automated more than 50% of travel claims, with zero human touch required.

These are not pilot programs. They are scaled, production-grade deployments. Trade Table uses AI to analyze images of damaged vehicles and produce repair estimates instantly, a transformation of auto claims that would have required days of manual assessment a few years ago.

Insurance Then vs. Now: How AI Changed the Game

A function-by-function comparison across underwriting, claims, customer service, and risk management — based on insights from Ozkan Okumus.

| Function | Traditional Approach | AI-Powered Approach |

|---|---|---|

| Underwriting |

Before Manual risk assessment using historical actuarial data; slow, batch-processing cycles |

Now AI models assess risk profiles in seconds using real-time, live data feeds |

| Claims Processing |

Before Weeks-long manual review; heavy documentation burden; adjuster-dependent |

Now Computer vision and NLP process damage images and documents automatically — Lemonade resolves some claims in seconds |

| Customer Service |

Before Call centres and paper forms; chatbot usage near 2% in early deployments |

Now AI chatbots handle 50%+ of queries; real-time app-based claim filing and agent chat |

| Personalization |

Before Broad demographic segmentation: age, income, postcode |

Now Behavioral data from wearables and IoT; dynamic premiums tied to lifestyle and driving habits |

| Risk Model |

Before Reactive — pay claims after a loss occurs; based on historical averages |

Now Predictive and preventive — AI identifies and reduces risk before losses happen |

| Data Sources |

Before Internal policy databases; census and actuarial tables |

Now Satellite feeds, IoT sensors, connected vehicles, health wearables, real-time pricing engines |

The Legacy System Problem

For many incumbent insurers, the path forward runs through a significant obstacle: technology infrastructure built 20 to 30 years ago and not designed for real-time analytics. Legacy systems are the single biggest challenge Okumus identifies. Cultural inertia among employees and a shortage of digital talent follow closely behind.

The solutions taking shape across the industry include migrating core systems to cloud-native platforms, forming partnerships with insuretech firms, and reskilling workforces from the inside. Generali’s digital academy, which upskills employees across all functions in data, AI, and customer experience, is one example of how major insurers are building internal capability alongside external partnerships.

The Three Disruptions That Will Define Insurance’s Next Decade

Ozkan Okumus identifies the forces that will reshape insurance within five to ten years — moving the industry from payer of losses to guardian of well-being.

Real-Time Adaptive Insurance

Premiums that change daily — or even hourly — based on live behavioral data. IoT devices, connected vehicles, and wearables feed continuous signals that update pricing in real time.

Usage-Based PricingInsurance as a Service

Flexible, subscription-based and embedded models — toggle coverage on when you need it, off when you don’t. Think Netflix or Amazon applied to risk protection.

Embedded & SubscriptionAI-Led Risk Prevention

Insurers shifting from responding to losses to preventing them. AI anticipates risk events before they occur, making the insurer an active guardian of customer well-being — not just a claims processor.

Predictive & PreventiveThe GCC should not just follow global insurance trends — it should set them. The digitalization, the government support, the sandbox frameworks are all there. The opportunity is to build from scratch what the rest of the world has to retrofit.

— Ozkan Okumus, Insurance Transformation Leader

Personalization, Data, and the Privacy Question

Personalization is no longer optional. Customers expect products that reflect their actual lives, not just their demographic profile. Lifestyle insurance now tracks steps, diet, and habits, adjusting premiums based on behavior. Tesla’s auto insurance adjusts rates in real time based on driving safety. These products rely on data from wearables, IoT devices, and connected platforms.

That data dependency raises legitimate privacy concerns. Okumus is clear: consent and transparency are non-negotiable. Customers need to know what data is being collected, how it will be used, and what benefit they receive in return. GDPR in Europe has pushed insurers toward privacy-by-design principles. Companies like Aiva offer clear opt-in processes and explain benefits upfront, treating data sharing as a transparent exchange rather than a buried terms-and-conditions clause.

What the GCC Should Do Next

For businesses across the GCC and MENA region, Okumus sees an opportunity unlike any other. The region’s advanced digitalization, government support for insuretech and fintech, and sandbox initiatives, particularly in the UAE, give GCC insurers the tools to build future-ready ecosystems from scratch rather than retrofitting decades of legacy infrastructure.

His advice is direct. Use regulation as a platform for innovation, not a constraint. Invest in digitally native talent. Build public-private ecosystems that connect government bodies, insurers, startups, and universities. The GCC has the infrastructure, the ambition, and the regulatory flexibility to move faster than most markets. The goal, as Okumus puts it, should not be to follow global insurance trends; it should be to set them.