Based on an Infoquest Expert Voices interview with San Sanghera, M&A Advisor and Former Head of Group Strategy, First Abu Dhabi Bank

Post-merger integration in the GCC is not simply a financial exercise. It is, above all, a human one. San Sanghera spent 30 years in GCC financial services, including 18 years at HSBC and 12 years as Head of Group Strategy at First Abu Dhabi Bank, where he sat at the center of the landmark FGB and National Bank of Abu Dhabi merger. He also led a cross-border acquisition completed entirely during the COVID lockdown. His takeaway, forged through both of those experiences, is direct: close the deal, and the real work has only just started.

Why Culture Defines Post-Merger Integration in the GCC

Few regions present as layered a cultural landscape as the GCC. Multiple nationalities, multi-generational family businesses, and national regulatory environments that vary meaningfully from country to country all converge inside a single transaction. San Sanghera is blunt about what happens when deal teams treat culture as secondary to financial and legal planning.

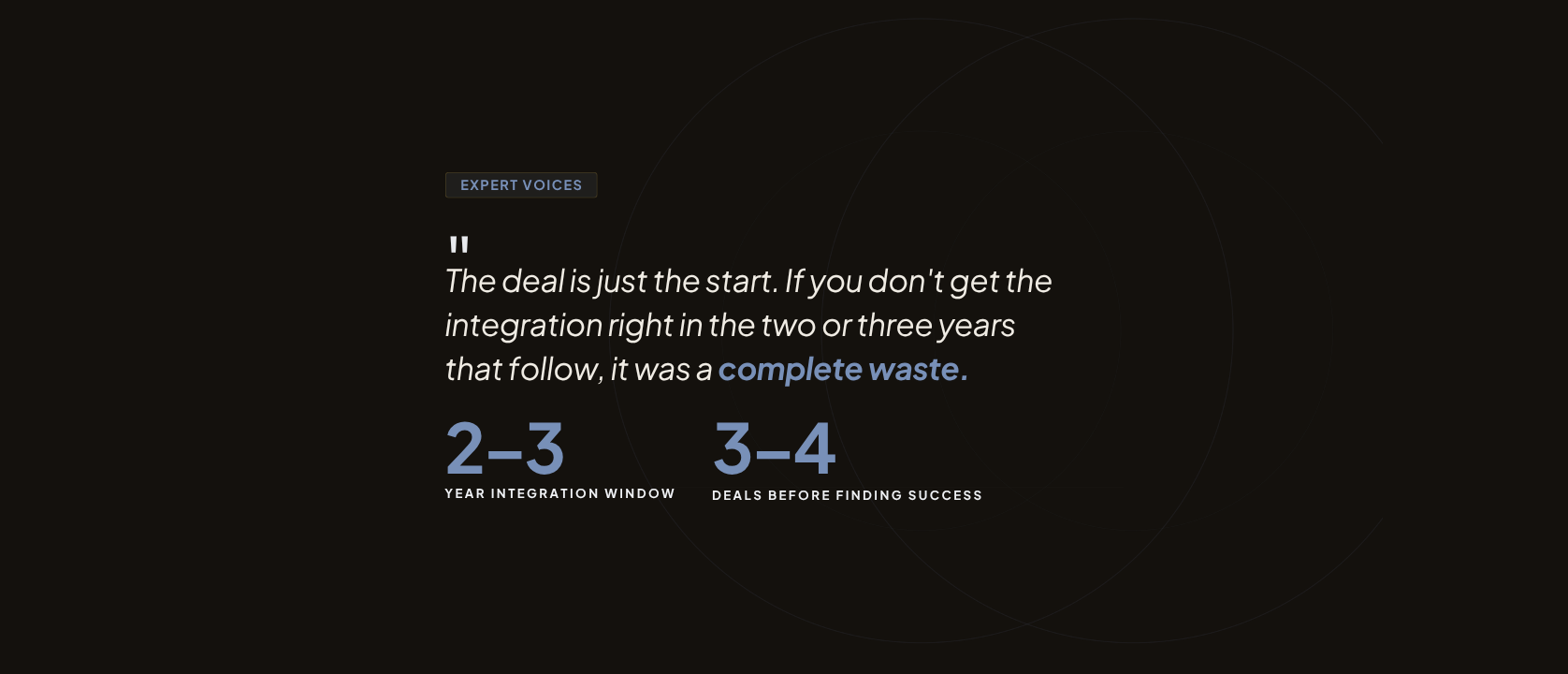

“If you go into an M&A not thinking about culture, you are gone,” he says. “You will fail. You may do the transaction, but your business will fail. The deal is just the start. If you don’t get the integration right in the two to three years that follow, it was a complete waste of time, money, and effort.”

The GCC does offer structural advantages. Availability of capital, both financial and human, is unmatched globally. The regional culture also supports large, consequential decisions in ways that not every market can. But that same decisiveness can accelerate failure just as quickly as success if the people dimension is ignored.

Merger of Equals vs. Takeover: Two Different Integration Challenges

San Sanghera draws a sharp line between a true merger of equals and a conventional takeover, and argues that conflating the two is itself an integration risk.

In a genuine merger, neither party’s culture should dominate. The goal is to build something new from two distinct inputs, and that requires deliberate, upfront work to define what the new organization’s culture will actually look like. “If you don’t do that,” he explains, “whichever culture was dominant will take over. A new culture is very rarely created without actively trying to create it.”

In a full takeover, the acquiring organization will inevitably exert pressure on the target’s culture. The risk there is different: losing the human capital that made the acquisition worth doing in the first place. Either way, the starting point is the same. Know the type of transaction you are running, and build your integration strategy accordingly.

Communication as the Number One Retention Tool in M&A

Across both transaction types, San Sanghera returns to one consistent theme: communication. It is, in his view, the single most important lever available to integration teams, and the one most frequently underused.

“The worst thing you can do is keep people in the dark,” he says. “You have to tell people everything, and tell them multiple times. When will their terms and conditions change? When will systems migrate? When might their job title change? If you don’t communicate that, the talent you are trying to acquire will walk, and that doesn’t help anybody.”

This applies whether the integration is a merger of equals or a straightforward takeover. Uncertainty breeds attrition. Clarity, even when the news is not entirely comfortable, builds trust. In high-stakes GCC transactions where retaining key personnel from the acquired entity often drives the deal’s strategic rationale, communication is not a soft skill. It is a core integration deliverable.

Setting Integration KPIs at Deal Inception, Not at the Finish Line

One of the most common integration failures San Sanghera observes is the belated arrival of performance metrics. KPIs that appear three-quarters of the way through an integration project are, in his view, a symptom of a deal that lacked strategic clarity from the start.

“You shouldn’t do an M&A unless you know why you’re doing it,” he says. “The KPIs need to be set at the beginning. Is it customer numbers? Profit? Market access? Number of products? That has to be the key metric. Everything else follows from there.”

He recommends organizing integration KPIs around four quadrants, echoing a classic balanced scorecard structure: process, customers, employees, and financials. Financial metrics tend to emerge naturally. It is the customer and people metrics that integration teams most often neglect, and their absence signals a fundamental gap in the integration plan.

The Four-Quadrant KPI Framework for Post-Merger Integration

Set integration metrics before the deal closes — not three-quarters of the way through

- Systems migration milestones met on schedule

- Operational process duplication eliminated

- Cross-entity workflow efficiency metrics

- Technology platform integration completion

- Customer retention rate post-close

- Net new customer acquisition against target

- Market access coverage achieved

- Cross-sell penetration into combined base

- Attrition rate of key talent from acquired entity

- Employee engagement scores across merged org

- Communication touchpoints delivered on schedule

- Cultural integration index (survey-based)

- Revenue synergies tracked against deal model

- Cost synergy realization rate and timeline

- Return on acquisition capital deployed

- Profit contribution from acquired entity

How AI Is Beginning to Reshape M&A in the GCC

San Sanghera sees three emerging roles for AI in the M&A process, none of which have yet reached full deployment, but all of which carry significant potential.

The first is due diligence. The document review phase of any major transaction is intensive and time-consuming. AI tools capable of scanning large volumes of documents, identifying anomalies, and flagging items for human review could compress this process dramatically. The second is legal drafting, where AI-generated first drafts of transaction documents could accelerate the negotiation phase and surface agreement and disagreement points earlier.

The third application is target identification. “If you can explain your own company to an AI agent and describe the ten characteristics you are looking for in a target, and it comes back with fifteen companies that match, the time saving is massive,” he says. He has not yet seen this deployed at scale in the GCC, but he believes it is coming, and that the region’s capital base and AI investment, particularly in the UAE, position it well to lead.

Three Pieces of Advice for Anyone Considering an Acquisition in the GCC

San Sanghera closes with three pieces of counsel shaped by three decades at the center of GCC M&A activity.

First: do not underestimate the complexity. Even deals that appear straightforward will surface complications. Getting expert advice early and listening to it is an investment that pays back many times over.

Second: protect the due diligence process. Do not allow deal timelines to compress the depth or quality of commercial and legal due diligence. The cost of cutting corners is always higher than the cost of getting it right.

Third: be prepared to walk away. The sunk cost fallacy is one of the most dangerous forces in any transaction. Being 75% through a deal does not obligate a buyer to complete it. “If something says it’s not right, walk away,” he says. “Too many people think M&A is easy. It is not. You should expect to explore three or four transactions before finding a successful one. Patience is part of the strategy.”