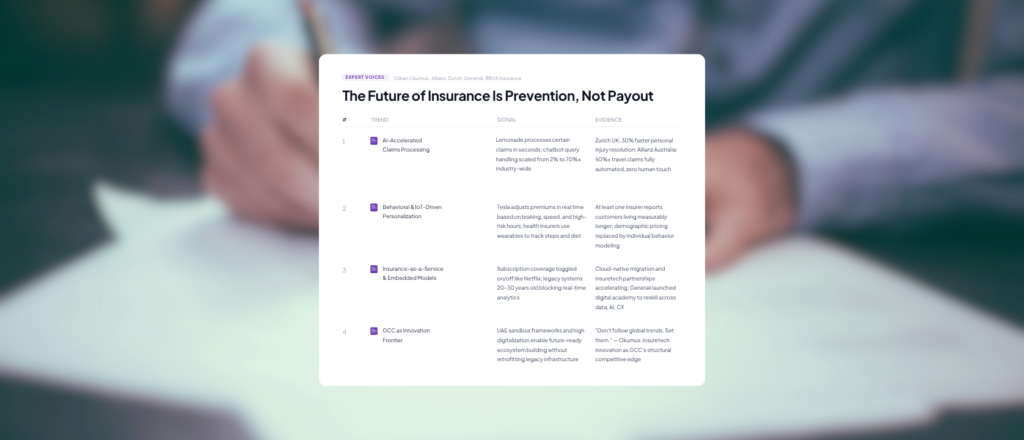

Based on an Infoquest Expert Voices interview with Ozkan Okumus, Insurance Transformation Leader

The conversation around GCC insurance trends is shifting fast. As climate volatility intensifies, digital commerce expands, and cyber threats multiply, the region’s insurers are being pushed to evolve well beyond traditional risk transfer. Ozkan Okumus, a leadership and transformation consultant who has held senior roles at Generali, Zurich, and Allianz across the Middle East, Turkey, and Australia, sees this moment as a genuine inflection point, one that the GCC is uniquely positioned to lead.

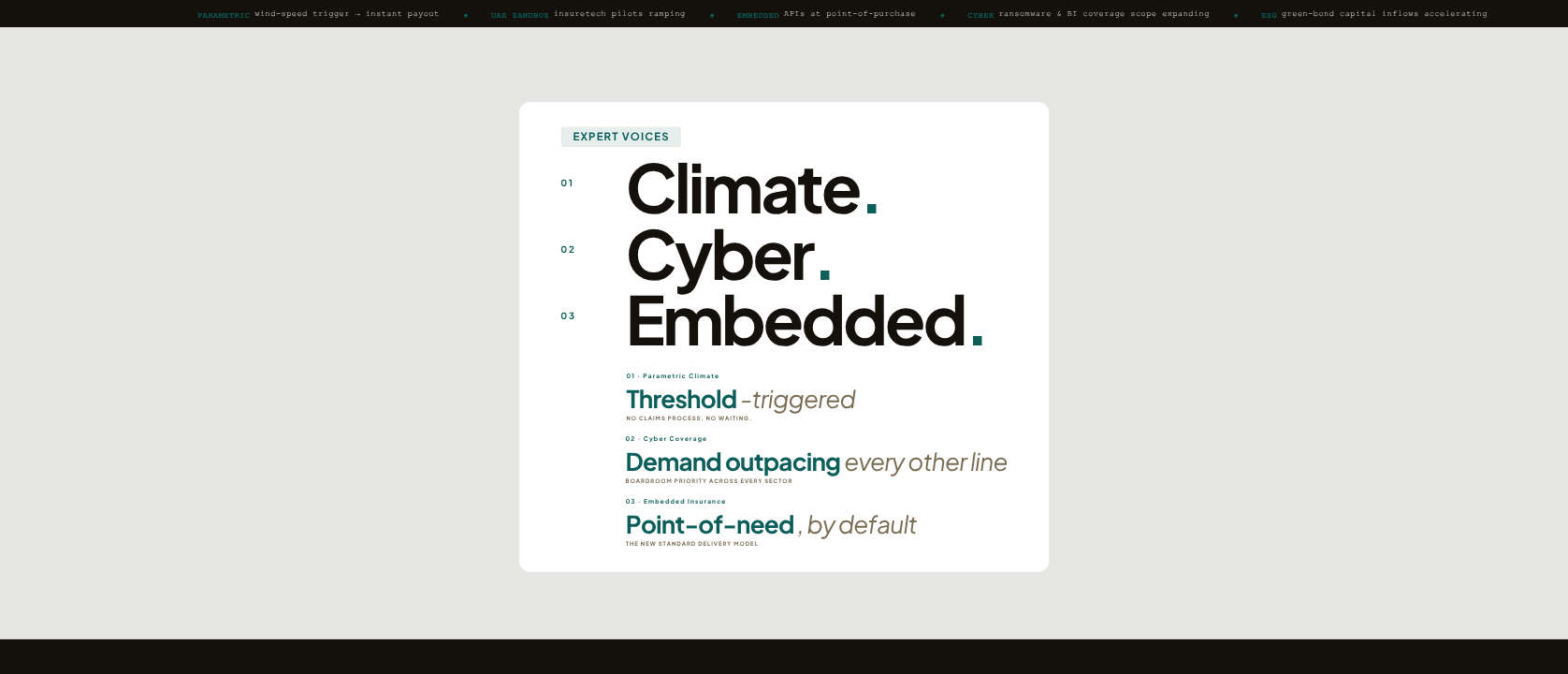

Parametric Climate Insurance Is Rewriting the Rulebook

The old model of climate insurance was reactive and slow. An event happened, documents were gathered, claims were reviewed, and eventually money changed hands. Parametric insurance breaks that cycle entirely. Instead of assessing damage after the fact, policies trigger automatically when a predefined threshold is crossed: a specific wind speed, a rainfall total, a temperature breach.

Okumus points to products that pay out automatically once set weather conditions are met as evidence that this model is no longer experimental. What makes it viable at scale is real-time data. Rather than relying on historical records, modern parametric policies draw on live satellite feeds to price flood and wildfire risk as conditions evolve. That capability requires sophisticated core systems, a significant investment, but a necessary one for any insurer serious about climate coverage.

For the GCC, the stakes are high. The region already faces extreme heat events and growing coastal flood exposure. An insurer that can price climate risk accurately, pay out quickly, and eliminate the bureaucratic claims process will have a genuine competitive advantage in markets where climate anxiety is rising.

Embedded Insurance Is Quietly Becoming the Default

When you buy a flight, you’re offered trip protection at checkout. When you take out a mortgage, unemployment coverage may come bundled in. When you rent a car, collision protection is included. This is embedded insurance, and Okumus is direct: it is rapidly becoming the standard delivery model, not the exception.

The mechanics rely on API-driven, plug-and-play pricing engines that slot seamlessly into a partner’s purchasing journey, a bank, an airline, an e-commerce platform. Coverage is offered at the point of need, in context, without a separate sales process. That removes one of the most persistent barriers in insurance adoption: people simply do not buy coverage they don’t think about until they need it.

By embedding protection into transactions consumers are already making, insurers reach people who would otherwise remain uninsured. In the GCC, where digital transactions are pervasive and consumer apps are deeply woven into daily life, the infrastructure for this model already exists. What remains is execution and partnership-building.

Cyber Insurance Demand Is Outpacing Every Other Line

Cyber risk has moved from a niche concern to a board-level priority across every sector. Okumus is clear about the trajectory: demand for cyber insurance is booming, and the scope of coverage is expanding. Policies now extend to ransomware attacks, data breaches, business interruption from system failures, and increasingly, reputational damage.

The GCC’s rapid digitalization makes this trend especially relevant. As more critical infrastructure, financial services, and government operations move online, the attack surface for bad actors grows with them. The question for regional insurers is not whether cyber coverage will become mainstream, it already is, but whether they can underwrite it with enough precision to make the business sustainable.

That requires access to threat intelligence data, underwriters who understand the technology landscape, and policy language flexible enough to keep pace with evolving attack vectors. Insurers that invest in those capabilities now will be better positioned as demand continues to climb.

Three Insurance Trends Reshaping the GCC

A side-by-side breakdown of climate, embedded, and cyber insurance

| Dimension | Parametric Climate | Embedded Insurance | Cyber Insurance |

|---|---|---|---|

| How it triggers | Automatically when a preset weather threshold is crossed (wind speed, rainfall, temperature) | At the point of purchase — bundled into a product, subscription, or credit agreement | Upon a confirmed cyber incident: ransomware, breach, business interruption, or reputational event |

| Key data source | Real-time satellite feeds and IoT weather sensors — not historical claims data | Partner transaction data and API-linked pricing engines | Threat intelligence feeds, incident logs, and security audit assessments |

| Core GCC opportunity | Price flood and extreme heat risk accurately as climate exposure grows in coastal and desert zones | Distribute through existing digital banking, e-commerce, and government service platforms | Protect rapidly digitalizing critical infrastructure, financial services, and government systems |

| Main implementation challenge | Core systems must support live data ingestion and real-time policy triggers | Requires plug-and-play APIs and real-time pricing engines across diverse partner environments | Underwriting precision requires skilled talent and access to evolving threat intelligence |

| Maturity level | Growing — moving from pilot to mainstream in climate-exposed markets | Accelerating — already standard in credit, travel, and e-commerce sectors | Booming — fastest-growing segment, driven by escalating attack frequency |

ESG Is No Longer Optional for Insurers

Environmental, Social, and Governance factors are becoming central to how insurers operate, and not just in terms of public positioning. Okumus notes that major multinationals are now refusing to underwrite fossil fuel projects and high-carbon industries. The price signal is deliberate: clean operations attract favorable rates, while heavy emitters face premiums that reflect their risk profile.

On the investment side, green bonds and green infrastructure are drawing significant insurer capital. GCC insurers are part of this movement. ESG-linked discounts for electric vehicles and green buildings are becoming increasingly common, and some multinationals operating in the region are already aligning their portfolios with net-zero commitments.

For companies in the GCC that still think of insurance as a pure cost center, this represents a meaningful shift. ESG performance is becoming a pricing variable, and the insurers willing to lead that conversation are gaining influence well beyond their traditional remit.

The GCC Insurance Innovation Framework

Three strategic pillars for regional insurers ready to lead, not follow

Use Regulation as a Platform for Innovation

Regulatory sandboxes are one of the GCC’s most underused assets. The UAE model allows insurers and insuretech firms to build and test products in a supervised environment — without full regulatory exposure.

- Engage directly with sandbox programmes (UAE, Saudi Arabia)

- Co-develop product prototypes with regulators, not after them

- Use pilot periods to stress-test parametric, embedded, and cyber products

Invest in Digital-Native Talent

The GCC has a young, tech-savvy workforce and a genuinely diversified talent pool. These are competitive advantages — but only if insurers actively invest in developing them rather than relying on imported expertise.

- Launch internal digital academies covering AI, data, and customer experience

- Build partnerships with universities for insuretech-focused programmes

- Create fast-track roles for digitally skilled local graduates

Build Cross-Sector Ecosystems

The GCC’s most durable advantage isn’t a single company or product — it’s the ability to build public-private systems that move faster than any individual player could alone.

- Create insuretech accelerators with government and academic partners

- Form structured alliances between insurers, startups, and banks

- Position the GCC as the originator of global insurance standards — not just the adopter

The GCC Should Be Setting Trends, Not Following Them

Okumus saved his sharpest observation for the close. The GCC, he argues, is in an enviable position: advanced digital infrastructure, digitally native young populations, and governments actively incentivizing innovation through sandbox frameworks. The UAE’s regulatory sandbox model, which allows insurers and insuretech firms to develop and test new products in a controlled environment, is a structure the entire region can build on.

His advice is practical and direct. Use regulation as a platform for innovation, not just a compliance requirement. Invest in the next generation of digital talent. Build cross-sector ecosystems that connect government, insurers, startups, and universities. The tools are already in place.

“Don’t just follow the global trends,” Okumus says. “Set them.” For a region with the infrastructure, the capital, and the political will to move quickly, that is less a challenge than a clear directive.